The silent war for strategic resources

At the heart of the technological and energy revolution, rare metals have become a key strategic lever for supporting green growth. From the electrification of transport to the digitalization of the economy, demand is soaring while supply remains concentrated in the hands of a few countries, first and foremost China. This structural imbalance—combining geopolitical dependency and ESG1 constraints—creates a major risk for global industrial sovereignty.

Analysis by the Investment team of Societe Generale Investment Solutions.

Why are rare earths unlike any other materials?

Lithium, nickel, cobalt, copper and rare earth elements such as neodymium and dysprosium form the foundations of the ongoing technological and energy transition. Electric vehicles, wind turbines and data centers all rely on these metals, whose unique properties (conductivity, magnetism, lightness) make them irreplaceable.

An F‑35 fighter jet requires more than 400 kilograms of rare earth elements, and an electric vehicle uses nearly four times more copper than a combustion‑engine car. In other words, the global energy transition rests on an essential yet fragile metallic foundation.

Despite their name, rare earths are not scarce by nature but by production economics. Found in often complex deposits, they require heavy, costly and often polluting extraction and refining processes. These industrial constraints make them strategic resources. As governments and companies commit to decarbonization, demand for these metals continues to accelerate, widening the structural imbalance between supply and future needs.

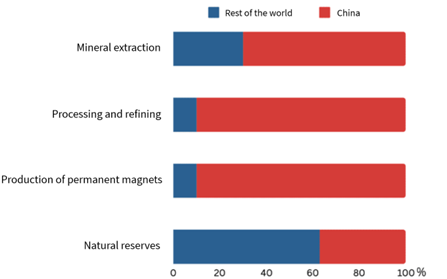

A market under pressure: dependency and structural imbalance

Global supply is concentrated among a limited number of players, led by China, which accounts for nearly 90% of refining capacity. This near‑structural dependency places Western economies in a position of strategic fragility: Europe, for example, imports 95% of its rare metals and has virtually no domestic refining capabilities.

Source: International Energy Agency (IEA)

At the same time, demand is surging, driven by the energy transition, transport electrification and digitalization. According to several studies, rare‑earth consumption could grow by nearly 8% per year over the coming decade. Even copper—long considered abundant—is becoming critical, with future needs expected to exceed current mining capacity by 2030.

Yet production is struggling to keep pace. Developing a mine often takes more than ten years, spanning exploration, permits and construction. In an environment with increasingly stringent ESG requirements, few players dare to invest heavily. The result is chronic under‑investment that is fueling price volatility.

A geopolitical dimension at the heart of the issue

Critical materials are no longer merely an industrial concern: they have become instruments of power. China, in a dominant position, has demonstrated its ability to use this leverage as an economic weapon. In 2010, Beijing suspended rare‑earth exports to Japan after a diplomatic dispute, triggering a global price spike. Under President Donald Trump, the US‑China trade war has revived these tensions, with China threatening to restrict deliveries of strategic metals to the United States.

In response, the United States is seeking to reinforce its mineral sovereignty. Donald Trump launched Project Vault, a strategic reserve of critical minerals backed by USD 12 billion, combining private capital and financing from the US Export‑Import Bank. Its aim is to stockpile materials such as gallium and cobalt to protect American industries from supply shocks. This initiative is part of a broader industrial revitalization strategy, alongside direct Pentagon investments in MP Materials and Lynas and massive incentives under the Inflation Reduction Act. The European Union, for its part, adopted the Critical Raw Materials Act in 2024, setting ambitious objectives for 2030: at least 10% of extraction, 40% of refining and 25% of recycling carried out within the EU.

Rare metals: the new oil of the 21st century?

Rare metals are no longer secondary resources—they have become the backbone of the global energy and digital transition. Their strategic importance, industrial scarcity and geopolitical weight make them a major investment theme.

While price volatility, environmental constraints and political tensions are creating a complex landscape, the structural growth dynamic remains strong. Beyond the metals themselves, the entire value chain—from extraction to recycling, including refining and equipment manufacturers—are playing a critical role in this sector’s momentum.

Furthermore, the growing integration of ESG criteria in the sector helps identify players genuinely committed to sustainable practices and the continuous improvement of their processes. States, companies and investors are thus now seeking to secure long‑term access to these essential resources, on which much of the world’s energy future depends.

Sources

(1) ESG: Environmental, Social and Governance

In a world in constant motion, where economic, social, and technological transitions are redefining business models,...

There seems to be an apparent contradiction between “transforming” money into lead and the ability to sell several...

In a context marked by declining interest rates, easier access to financing, and a recovery in transactions, the outlook...

In a context marked by declining interest rates, easier access to financing, and a recovery in transactions, the outlook...